Last week, the Federal Reserve announced the implementation plan of the second quantitative easing, the asset purchase quota was slightly higher than expected, and the globally more abundant liquidity will continue to push up the price of resource products. However, in the short term, the European CDS price rose sharply or induce debt problems to re-float. Out of the water, it will trigger zinc price adjustments.

Last week, the Federal Reserve announced the implementation plan of the second quantitative easing, the asset purchase quota was slightly higher than expected, and the globally more abundant liquidity will continue to push up the price of resource products. However, in the short term, the European CDS price rose sharply or induce debt problems to re-float. Out of the water, it will trigger zinc price adjustments. The Fed’s “secondary quantitative easing†was slightly larger than expected. On Thursday, the Fed announced the implementation plan of the second quantitative easing policy. This round of the 600 billion U.S. dollar government bond purchase plan will be maintained at a monthly rate of 75 billion U.S. dollars for eight months. The Fed also said that it will regularly review the progress and scale of government bond purchases to help maximize employment and maintain price stability.

However, the second time there was a difference between quantitative easing and the first time. First of all, the second quantitative easing has been greatly reduced, and the market impact has been weakened. The scale of the first quantitative easing policy launched at the end of 2008 was 200 billion U.S. dollars, and the second quantitative easing launched last week was 600 billion U.S. dollars, which is far less than the total amount of the first quantitative easing. At the same time, the market had long been rumored that the size of the second quantitative easing was between 500 billion and 1,000 billion US dollars, making investors sell US dollar assets on a large scale. Therefore, bad news may have been reflected in the market in advance.

Second, the goals of the two quantitative easing programs are different. The first quantitative easing was launched with the continuous deepening of the subprime mortgage crisis and the continuous increase in the financial system's collapse risk. Its purpose was to stabilize the banking system; the second quantitative easing was launched after the economy stabilized and unemployment ceased. In the case of high rates, it was introduced to improve the job market. Therefore, the first time quantitative easing was large in scale, and it was urgently used to effectively reverse the effects of arrogance; the second quantitative easing was smaller in scale and slower to be withdrawn in order to trigger appropriate inflation and improve the employment rate.

Again, the duration of the two quantitative easing is different. The first quantitative easing focuses more on the short-term effect and avoids the rapid collapse of the financial system. The second quantitative easing is a gradual and gradual progress. If the U.S. employment rate does not improve significantly, the Fed may implement the third and fourth quantitative easing policies until the unemployment rate returns to normal levels. In October, the unemployment rate in the United States continued to remain at a high of 9.6%. According to past experience, to reduce the unemployment rate to about 5%, the implementation of quantitative easing may continue for many years.

In the short term, the introduction of the second quantitative easing has been digested by the market in advance. After the US dollar index rose to 88.71 in June, it continued to fall to the current level of 77. It is expected that this is an early reflection of investors' expectations for the second quantitative easing and even three quantitative easing. If the short-term U.S. dollar index falls again, it will be less likely to stimulate zinc prices.

In the long run, the introduction of the second quantitative easing will inject large amounts of funds into the market. As the United States and the developed countries of Europe are undergoing a difficult deleveraging process, the US economy does not have enough capacity to digest the huge amount of capital of the second quantitative easing. This will inevitably divert some of the funds to developing countries (especially China) represented by the “BRIC countries†with a high rate of return on capital, pushing up the prices of domestic assets and financial products.

After the CDS rose, or once again "ignited" the European debt problem, the expectation of the second quantitative easing of the Fed was honored, the market focus once again shifted to the euro zone. Recently, bond yields in many countries in Europe hit a new high since the establishment of the euro zone. Market investors expect the risk of European debt defaults to increase, causing investor concerns.

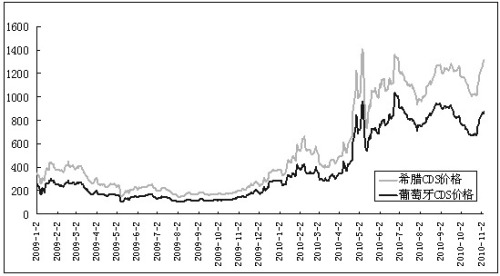

CDS, also known as credit default swaps, is a derivative product that occurs between two counterparties, similar to insurance against bond defaults. Buyers of CDS usually pay sellers to buy certain kinds of bonds. If they breach the contract, they can get compensation from the seller. The higher the price, the greater the possibility that the two parties believe that the bond defaults. The chart above shows that since mid-October, the price of credit default swaps in Greece, Portugal, Ireland and other countries has continued to rise. Last week, the cost of default insurance on Irish government bonds and the country’s national bond yields hit a record high, and credit default swaps also set a record high for several consecutive days and set a new record high since the establishment of the euro zone last Friday. .

Influenced by the fiscal austerity policy triggered by the debt crisis, the level of economic development in the euro zone countries has become more differentiated. Countries with high savings rates, such as Germany and France, have maintained rapid growth, while countries such as Ireland, Greece and Spain have continued to struggle in difficult circumstances. Because there is no practical plan to stimulate economic recovery, European debt can hardly be solved fundamentally. If CDS prices continue to rise significantly, it will rekindle the European debt crisis and trigger a sharp adjustment in the prices of risky assets.

To sum up, in the long term, the Fed’s “quantitative easing†will inject large amounts of funds into the market. Abundant liquidity will continue to push up global asset prices. On the other hand, the US irresponsible monetary policy Will undermine the long-term purchasing power of the dollar, making dollar-denominated commodity prices have been boosted, thereby supporting zinc prices. In the short term, CDS prices in Greece, Portugal, and other countries have risen sharply, credit default risk is deteriorating, and the second round of “European debt crisis†is looming. It is expected that Shanghai Zinc will continue to adjust or even make downward corrections in the near future. After the adjustment, it is expected to continue rising.

pvc interior door panel

FOSHAN GAOMING JIALESHI DECORATIVE MATERIAL CO.,LTD , http://www.jlsbuildingmaterial.com